Blog

What Is a Charitable Remainder Unitrust (CRUT) and When Do You Need an Appraisal?

A charitable remainder unitrust (CRUT) pays you or another beneficiary a variable income stream for life or up to 20 years, then leaves the remainder to charity. This guide explains the IRC Section 664 payout rules and exactly when funding a CRUT with property triggers a qualified appraisal and IRS Form 8283.

What Is a Charitable Remainder Unitrust (CRUT)?

A charitable remainder unitrust is an irrevocable trust that pays you, or another named beneficiary, a variable percentage of the trust's assets every year, then transfers whatever remains to a qualified charity at the end of the term. It is a split-interest gift: part of the property's value supports an income beneficiary, and part is earmarked for charity from the day the trust is signed.

Under 26 U.S. Code Section 664, a CRUT must pay out annually for the life of one or more individual beneficiaries (who must be living when the trust is created) or for a fixed term of no more than 20 years. Once that term ends, the remaining trust principal passes to one or more Section 170(c) charitable organizations. The IRS's charitable remainder trust guidance confirms this structure and notes that the trust must file Form 5227 annually to report its income, distributions, and remaining charitable interest.

The defining feature of a unitrust, as opposed to other split-interest vehicles, is that the payout is revalued every year. The trustee determines the fair market value of trust assets annually, and the income beneficiary receives a fixed percentage of that new value, not a flat dollar amount locked in at funding.

Why the Annual Revaluation Matters

Because the payout is a percentage of current value rather than a fixed sum, a CRUT's income stream rises when trust investments perform well and falls when they don't. Treasury regulations describe this mechanic in detail, including the specific valuation methods trustees must use each year and the timing rules for when payments are considered made (Treas. Reg. Section 1.664-3). This variability is the tradeoff donors accept in exchange for potential growth in their income over time.

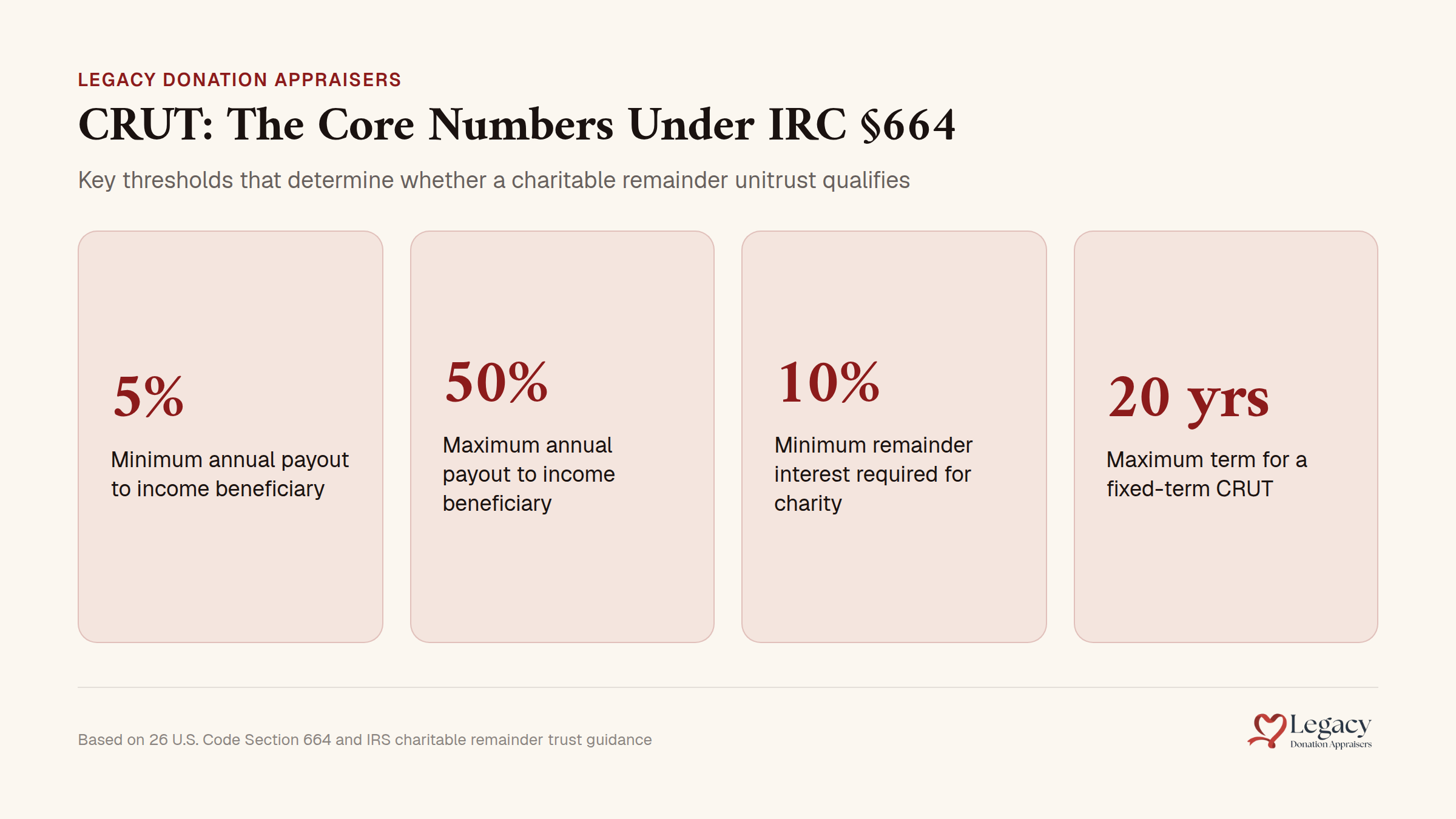

How the 5%-50% Payout Rule and 10% Remainder Requirement Work

A CRUT's annual payout to the income beneficiary must fall between 5% and 50% of the trust's net fair market value, revalued each year, and the trust must be structured so that charity's projected remainder interest is worth at least 10% of the initial contribution.

Section 664(d)(2) sets the payout percentage boundary directly: the fixed percentage the trust distributes each year cannot be less than 5% or more than 50% of the trust's annually valued net assets (26 U.S. Code Section 664). Set the percentage too low and the trust fails to qualify; set it too high and it starts to look like the donor never really gave anything away.

The second guardrail is the 10% minimum remainder interest. The IRS's CRT guidance states plainly that the remainder donated to charity must be at least 10% of the initial net fair market value of all property placed in the trust. This is an actuarial calculation performed at the time the trust is funded, using the chosen payout percentage, the beneficiary's age or the trust's term, and IRS actuarial tables. A CRUT that pays out too generously to the income beneficiary, over too long a term, can fail this test before it ever gets off the ground.

Watch out: These two rules interact. A higher payout percentage or a longer term reduces the projected value of what's left for charity. If a proposed CRUT structure doesn't clear the 10% floor, the trust document has to be adjusted (a lower percentage, a shorter term, or an older income beneficiary) before it can be funded.

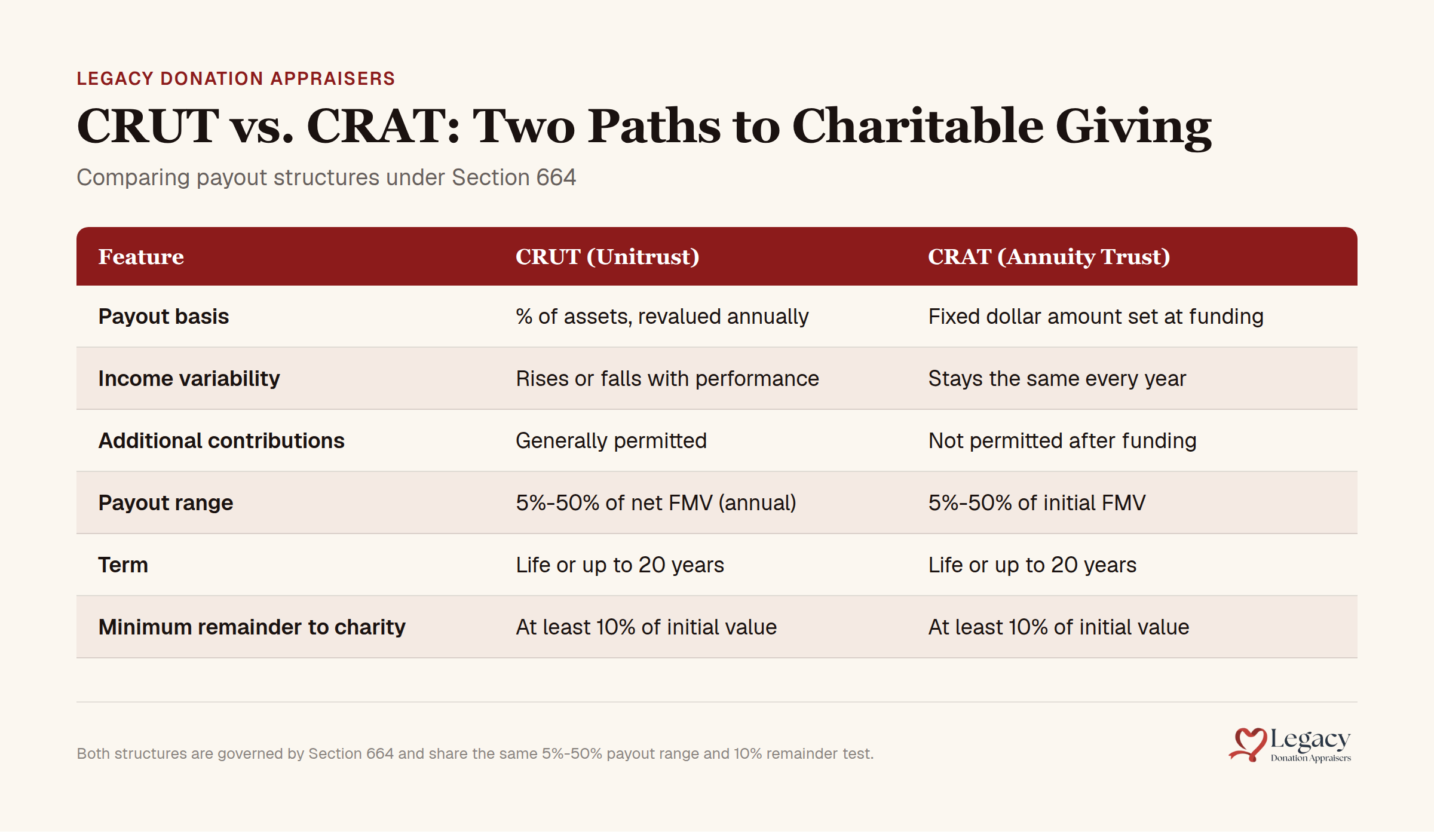

CRUT vs. CRAT: Variable Unitrust vs. Fixed Annuity

A charitable remainder unitrust pays a variable amount based on annual revaluation, while its close cousin, the charitable remainder annuity trust (CRAT), pays a fixed dollar amount set once at funding. Both are governed by Section 664 and both require the same 5%-50% payout range and 10% remainder test, but the income mechanics work differently.

Feature | CRUT (Unitrust) | CRAT (Annuity Trust) |

|---|---|---|

Payout basis | Percentage of assets, revalued annually | Fixed dollar amount set at funding |

Income variability | Rises or falls with trust performance | Stays the same every year |

Additional contributions | Generally permitted | Not permitted after initial funding |

Payout range | 5% to 50% of net fair market value | 5% to 50% of initial fair market value |

Term | Life or up to 20 years | Life or up to 20 years |

Minimum remainder to charity | At least 10% of initial value | At least 10% of initial value |

Donors who want a hedge against inflation, or who expect trust assets to appreciate meaningfully, tend to favor the unitrust structure precisely because the payout can grow. Donors who want payment certainty for budgeting purposes sometimes prefer the annuity trust instead. Neither is inherently better; the right choice depends on the donor's income needs and the asset being contributed.

When Does Funding a CRUT Trigger a Qualified Appraisal and Form 8283?

Funding a CRUT with non-cash, non-publicly-traded property, such as real estate, a closely held business interest, art, or equipment, triggers a qualified appraisal requirement and IRS Form 8283 whenever the claimed value of the contributed property exceeds $5,000.

This rule doesn't come from Section 664 itself. It comes from Section 170(f)(11) and the instructions to Form 8283, which govern noncash charitable contributions generally. A gift into a CRUT is still a charitable contribution of property, and the IRS treats it the same way it treats any other donation of appreciated, illiquid assets:

Real estate: Rental property, land, or a former residence contributed to a CRUT needs a qualified appraisal before the return claiming the deduction is filed.

Closely held business interests: Stock in a non-public company, or an LLC or partnership interest, requires an appraisal because there's no public market quote to rely on.

Art and collectibles: Paintings, sculpture, and similar property need a qualified appraisal, and the IRS pays close attention to art valuations claimed above certain thresholds.

Equipment and other tangible personal property: Machinery, vehicles, and similar business assets follow the same $5,000 rule once contributed at claimed fair market value.

Publicly traded securities are the exception. Because their value is readily available from daily market quotations, contributing publicly traded stock to a CRUT generally does not require a qualified appraisal, even though Form 8283 may still need to be filed depending on the total amount of noncash contributions claimed for the year.

When an appraisal is required, Form 8283 Section B must be completed and attached to the donor's return, and it must include the appraiser's signature and identifying information. Our guide on what the IRS rules are for donations over $5,000 walks through the mechanics of that threshold in more detail.

Pro tip: Get the appraisal done well before the trust is funded and the return is filed. A qualified appraisal must be received before the due date, including extensions, of the return on which the deduction is first claimed. Waiting until tax season to find an appraiser for a piece of real estate or a business interest is a common, avoidable delay.

What the Appraisal Values, and What It Doesn't

The qualified appraisal establishes the fair market value of the property itself, not the deductible portion of the gift. A separate actuarial calculation, using IRS Section 7520 tables, then determines what percentage of that fair market value counts as the deductible remainder interest.

These are two distinct steps, and donors sometimes conflate them. The appraiser's job stops at the property: what is this parcel of land, this business interest, this painting, actually worth on the open market as of the contribution date. From there, the trustee or the donor's tax advisor applies the CRUT's payout percentage, term, and the beneficiary's age (or the fixed term of years) to IRS actuarial factors to compute the present value of the charitable remainder interest. That present value, not the full appraised value of the property, is what flows through to the charitable deduction calculation.

Example: A donor contributes a commercial building appraised at $500,000 into a CRUT paying 6% for 15 years. The appraisal establishes the $500,000 fair market value. The actuarial math (based on the payout rate, term, and applicable federal rate) might determine that the present value of the remainder interest is $210,000. That $210,000 figure, not the full $500,000, is the number that matters for the charitable deduction, though the appraisal of the underlying property is still what makes the entire calculation defensible.

Key takeaway: A qualified appraisal supports the property's value. It does not calculate the deduction. Anyone telling you the appraisal itself produces your tax deduction figure is skipping a step.

Why Donors Choose a CRUT

Donors typically fund a CRUT with an appreciated asset for three reasons working together: an ongoing income stream, a partial charitable deduction in the year of funding, and the ability to avoid immediate capital gains tax on the contributed asset's appreciation.

When a donor sells an appreciated asset outright, capital gains tax is due on the sale in that same year. When the same asset is instead contributed to a CRUT, the trust (as a tax-exempt entity) can sell the asset and reinvest the full proceeds without immediate capital gains tax at the trust level, while the donor receives a partial charitable deduction based on the present value of the remainder interest calculated under Section 664 (IRS CRT guidance). The donor's basis in property contributed to the trust generally carries over, and payments received from the trust are taxed to the beneficiary under ordering rules set out in the regulations.

This structure tends to appeal most to donors holding a single large, low-basis, illiquid asset (a piece of real estate held for decades, a stake in a family business, a significant art collection) who want to convert that concentrated position into diversified income without a one-time tax hit on the sale.

FAQ

Q: Do I need a qualified appraisal for every asset I contribute to a CRUT? Not for publicly traded securities, since their value is set by the market. For real estate, closely held business interests, art, equipment, and most other non-cash property, a qualified appraisal is required once the claimed value exceeds $5,000.

Q: Who can perform the appraisal for a CRUT contribution? The appraisal must be completed by a qualified appraiser, generally someone credentialed through an organization such as the American Society of Appraisers or a comparable body, following the Uniform Standards of Professional Appraisal Practice published by The Appraisal Foundation.

Q: Does the appraisal determine my tax deduction amount? No. The appraisal establishes the fair market value of the property. A separate actuarial calculation under Section 664, using the trust's payout rate and term, determines what portion of that value counts as the deductible remainder interest.

Q: What form do I attach to my tax return? When a qualified appraisal is required, Form 8283 Section B must be completed, signed by the appraiser, and attached to the donor's return. See our overview of what the IRS rules are for donations over $5,000 for the filing details.

Getting the Appraisal Right Before You Fund the Trust

A CRUT can be a powerful way to turn a concentrated, appreciated asset into lifetime income and a future charitable gift, but the structure only works if the underlying appraisal is defensible. An inflated or unsupported valuation puts the entire deduction, and the trust's compliance with the 10% remainder test, at risk.

Our team prepares charitable donation appraisals for the exact assets that typically fund a CRUT, including real estate and personal property, fine art, machinery and equipment, and closely held business interests. Every report is prepared in accordance with USPAP and structured to meet IRS Form 8283 requirements before your return is due. If you're planning to fund a charitable remainder unitrust with an appreciated asset, request an appraisal early so your trustee and tax advisor have the fair market value they need to run the actuarial numbers with confidence.

This article is provided for general informational purposes only and does not constitute legal, tax, or financial advice. Readers should consult a qualified attorney or CPA regarding their specific circumstances.