★★★★★

Exceeded my expectations in every way! They were extremely prompt, incredibly friendly, and remarkably affordable.

IRS-qualified appraisals prepared for tax deductions and Form 8283 filings. Get defensible fair market valuations for your non-cash charitable contributions of personal property, equipment, vehicles & boats, and business interests.

A qualified appraisal is a formal valuation report that meets specific IRS requirements under Treasury Regulation Section 1.170A-17. When you claim a deduction of more than $5,000 for non-cash charitable contributions, the IRS requires a qualified appraisal prepared by a qualified appraiser to substantiate the claimed fair market value.

The appraisal must be prepared in accordance with the Uniform Standards of Professional Appraisal Practice (USPAP) and include detailed information about the property, valuation methodology, and the appraiser's credentials. For donations exceeding $5,000, you must complete Section B of IRS Form 8283 and have your appraiser complete and sign Part IV (Appraiser Declaration).

Under IRS regulations, a qualified appraiser must meet several criteria:

Legacy Donation Appraisers works with credentialed professionals holding recognized designations such as ISA (International Society of Appraisers), ASA (American Society of Appraisers), and AAA (American Society of Appraisers), ensuring your appraisal meets all IRS requirements.

The IRS imposes strict timing requirements on qualified appraisals:

If your donation occurs outside the 60-day window from the appraisal date, the report may need to be updated to reflect the correct valuation effective date. Planning ahead ensures compliance and avoids potential issues with the IRS.

Legacy Donation Appraisers provides IRS-qualified appraisals across all major asset categories for charitable tax deductions, including:

Appraisals of furniture, jewelry, watches, collectibles, antiques, luxury goods, clothing, decorative arts, and household inventory.

Appraisals of paintings, prints, sculpture, photography, and mixed media by Old Master, Impressionist, Modern, Post-War, and Contemporary artists.

Appraisals of manufacturing equipment, construction machinery, restaurant equipment, medical devices, agricultural equipment, and specialized tools.

Appraisals of privately held business interests, including S Corps, C Corps, LLCs, ESOP-owned companies, and partnership interests.

Appraisals of retail and wholesale inventory, including food inventory, clothing and apparel inventory, raw materials, and finished goods.

Appraisals of gold, silver, platinum, bullion bars, investment-grade coins, and precious metal holdings.

Appraisals of cars, trucks, SUVs, classic vehicles, boats, RVs, motorcycles, and specialty vehicles.

Appraisals of digital assets including Bitcoin, Ethereum, stablecoins, NFTs, and other blockchain-based holdings.

Pricing for qualified appraisals varies based on several factors:

We provide transparent fixed-fee quotes prior to engagement so you understand costs upfront. The typical process includes:

Turnaround time depends on asset complexity and documentation completeness, with many standard assignments completed within several business days.

Exceeded my expectations in every way! They were extremely prompt, incredibly friendly, and remarkably affordable.

Very helpful and professional! I have searched for appraisers before and it's been hard to find someone who can manage complex projects. The items I donated covered many SKUs and Joe has managed to help me value them quickly and accurately! The team provided me with all necessary documents so I could submit with my tax return. Very pleasant experience with him and highly recommend!

I'd have given them 10 stars if it were possible. They were quick to reply, incredibly helpful, knowledgeable, professional and managed to make it fairly simple. I highly recommend them!

The best company I was lucky to find by accident. Their customer service is OUTSTANDING and a welcome surprise in today's world where good customer service is an anomaly! They returned an appraisal in a timely manner, it was clear, concise, cost-effective and exactly what I needed. My CPA is also thrilled to have them as an accredited appraisal service he can use for other clients. I rarely leave reviews, but I could not pass giving them 5 stars and I'd give 10 if possible!

We were very satisfied with the results - fast and efficient communication, understanding our company's needs, on-time delivery of the report, as well as reasonable price point. Highly recommend.

Professional & responsive. The report was quite thorough as well.

Where we work

We provide on-site and remote appraisal services across the following locations.

From Our Blog

Guides on IRS Form 8283, donation deduction rules, art and ticket donations, and the appraisal penalties to avoid.

A charitable remainder unitrust (CRUT) pays you or another beneficiary a variable income stream for life or up to 20 years, then leaves the remainder to charity. This guide explains the IRC Section 664 payout rules and exactly when funding a CRUT with property triggers a qualified appraisal and IRS Form 8283.

Read more →

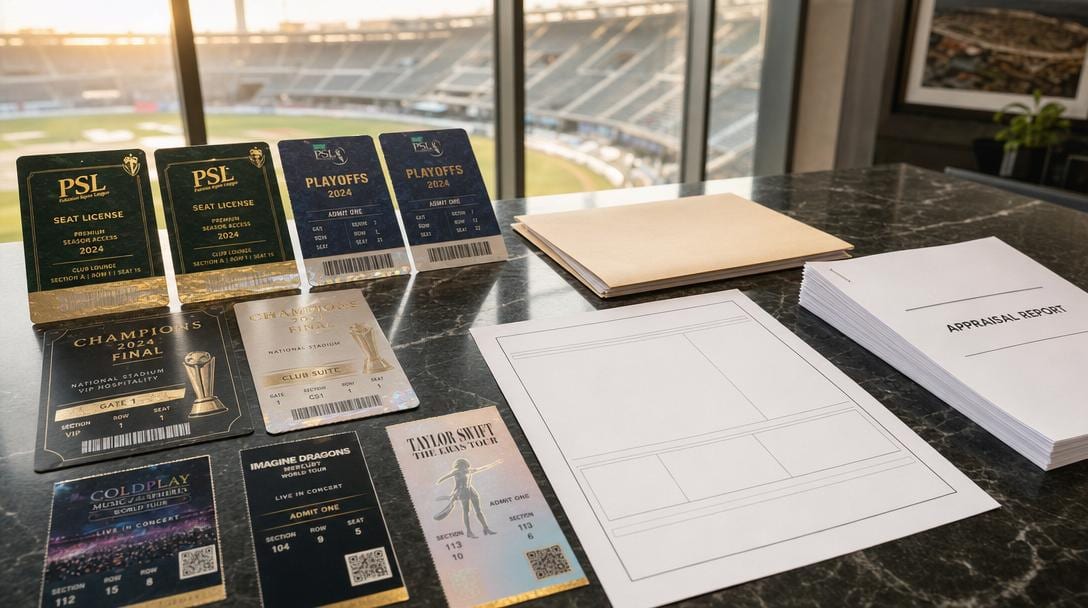

Donating sports or event tickets to charity can generate a meaningful tax deduction, but the IRS requires a qualified appraisal for donations over $5,000 and strict compliance with Form 8283. This guide covers the exact thresholds, how fair market value is determined, what a compliant appraisal report must contain, and the deadlines you cannot miss.

Read more →

Intuit has retired ItsDeductible, leaving donors without their go-to tool for valuing non-cash charitable contributions. This guide covers the best alternatives, from dedicated tracking apps like Deductible Duck and DeductAble to free charity guides and IRS-required qualified appraisals, so you can protect every deduction you claim.

Read more →

IRS promoter penalties for charitable donations can fall on appraisers, not just promoters, under IRC sections 6700, 6701, and 6695A. This guide breaks down how each penalty is triggered, how the math works, and what separates a defensible appraisal from a costly one.

Read more →

The IRS has placed art donation deductions on its 2026 Dirty Dozen list, signaling aggressive enforcement against inflated valuations and promoter-driven schemes. This guide covers the exact thresholds, appraisal requirements, penalty exposure, and what to do if you have a past or planned art donation.

Read more →

A practical guide to understanding when a qualified appraisal is legally required — and how to protect your deduction

Read more →See all frequently asked questions here

A qualified appraisal is required when you claim a deduction of more than $5,000 for non-cash property other than certain publicly traded securities. For donations under $5,000, you may not need a formal appraisal but should still maintain documentation supporting your claimed value. The appraisal must be prepared by a qualified appraiser and meet IRS requirements under Treasury Regulation Section 1.170A-17.

A qualified appraisal must meet specific IRS requirements: be prepared in accordance with USPAP standards, completed by a qualified appraiser, include a detailed property description and condition, state the valuation effective date, explain the valuation methodology, provide the appraiser's credentials and competency declaration, state the fair market value as defined under IRS regulations, and be prepared for income tax purposes. The appraisal must also be performed within 60 days before the donation date.

Cost varies based on asset type, number of items, complexity, and reporting requirements. Factors include asset category and valuation complexity, number of items being appraised, Section B reporting requirements, need for additional documentation such as artwork valued at $20,000 or more, and business or illiquid asset analysis. We provide transparent fixed-fee quotes prior to engagement so clients understand costs upfront.

The appraisal must be performed no earlier than 60 days before the date of contribution and no later than the due date including extensions of the tax return on which the deduction is first claimed. If the donation occurs outside the 60-day window from the appraisal date, the report may need to be updated to reflect the correct valuation effective date.

Under IRS regulations, a qualified appraiser must hold recognized appraisal credentials or meet required education and experience standards, regularly prepare appraisals for compensation, demonstrate competency in valuing the specific property type, provide their taxpayer identification number, not be the donor, donee, or a related party, and not charge a fee based on a percentage of the appraised value.

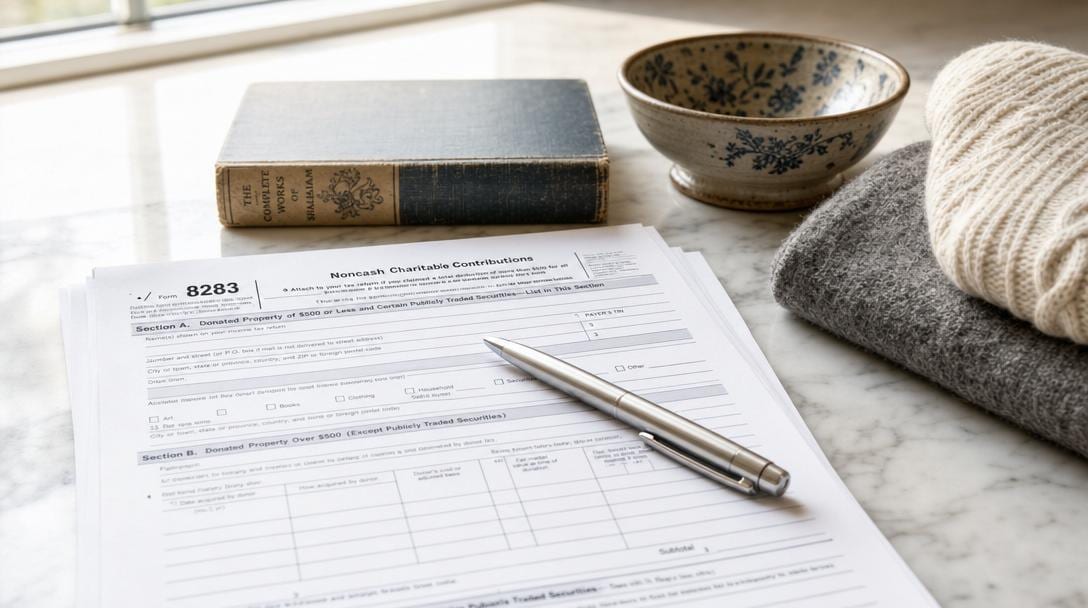

IRS Form 8283, Noncash Charitable Contributions, is used to report non-cash donations exceeding $500. When the claimed deduction exceeds $5,000, Section B must be completed and supported by a qualified appraisal. The form documents the property description, acquisition and donation dates, manner of acquisition, fair market value, donee acknowledgment, and qualified appraiser declaration.

We prepare qualified appraisals for a wide range of donated assets including personal property, fine art, machinery and equipment, business interests, inventory, bullion and precious metals, vehicles, and cryptocurrency. Each asset type requires specialized expertise and market knowledge to determine accurate fair market value.

Yes, we offer expedited appraisal services to help donors and advisors meet IRS filing deadlines, including support for Form 8283 Section B. Rush availability depends on asset type, complexity, and documentation readiness, so early coordination is recommended.

Get started with your IRS-qualified charitable donation appraisal